On a regular basis, we publish election countdown briefing notes thoroughly dissecting factors that may have an impact on the overall 2024 elections but more importantly on the results thereof. The range of issues we cover include but are not limited to party specific issues, funding, policy issues, voter turnout, IEC preparations and coalitions. The overarching aim of these notes is to provide clients with ahead of the curve insights on several aspects of the elections and their impact.

It was widely expected that the ANC would lose its majority nationally and in KZN and Gauteng in the May elections – an issue that we have been speaking about as far back as early 2023. What was a shock was the extent of the party’s decline. In this note, we provide a summary of the outcome of the elections and reflect on the results by delving into some key insights that the elections data provide. In particular, we are interested in the potential implications of these results for the 2026 local government elections and the 2029 national and provincial elections. As by-elections indicated prior to the May elections, the MK Party took votes from all the big competitors in KZN (ANC, IFP, EFF and DA). If the party is able to maintain the momentum it has built until the 2026 elections, we can expect it to win an outright majority in the eThekwini metro. In metros generally, we observe a decline of both the ANC and the DA and several other parties, including ActionSA. This points towards a fragmentation of the system and could mean that the country may not have a dominant party in the foreseeable future.

While the history of coalitions in the country can be traced back to the early days of democracy, the phenomenon gained some prominence after the 2016 local government elections and became an established part of the political system after the 2021 local government elections. As such, the country’s experience of coalitions (at least in recent years) has been restricted to the local government sphere. Given our expectation of coalitions at national and provincial level after May 29, we discuss valuable lessons that can be learnt from the experience of metropolitan municipalities with coalitions. It is evident that written coalition agreements hold no value and flexibility is needed – the failure of DA-led coalitions demonstrate this; smaller parties can easily be swayed by the promise of more powerful positions – the ANC-EFF takeover in Johannesburg and Nelson Mandela Bay supports this point; club deals are more workable – this is demonstrated by the relative longevity of ANC-EFF coalitions in Gauteng metros; and as formerly DA-led coalitions in Johannesburg and Nelson Mandela Bay demonstrate, coalitions with many smaller party partners are prone to instability.

At national level, parties need solid agreements which allocate acceptable levels of power to smaller partners in order to avoid defections. Fortunately, at this level there is enough inconsequential power to distribute among smaller parties who will be keen on joining coalitions given their limited chance of ever winning an outright majority. This will allow the bigger partners, most likely the ANC, to maintain the status quo in the policy space.

The market overall expected an ANC print in the region of 45.5% and sees mixed risks around this (sellside to upside, buyside balanced) and the prospects of some positive momentum in policy reforms, as well as a positive market reaction post-elections. The market sees the coalition lasting the complete term if not into the 2026 elections (perhaps too positive a view) and that an ANC-IFP-smaller party outcome is most likely though the ANC majority gets a small showing as does confidence and supply. Very low probabilities are assigned to EFF inclusion. Markets see coalitions lasting at least two years if not the full term of five years though other respondents were much more sceptical (and the offshore buyside more than other market participants). Markets see the DA above 50% in the WC with a small margin, and the ANC around 37.4% in Gauteng and 34.0% in KZN. There were broad expectations of neutral to positive reform momentum and similarly a broad market consensus on a positive reaction to the elections.

Follow the maths. This is a seminal election where the maths of coalitions is going to be exceptionally tight. We do not see any “easy” routes here to magically higher growth or coalition stability. Instead, we must consider the most likely and least unstable options. An ANC-IFP-smaller party coalition remains the baseline but is only of moderate probability given that the IFP will need in effect to change its current stance that it wants a grand coalition – the ANC could offer them the KZN Premiership in this respect. If this doesn’t work, we think an ANC-DA or grand coalition (ANC-DA-IFP) could be possible though we need to consider what works in the provinces and Gauteng especially (this would). This means we must remain cognisant of the DA needing some involvement. We do not see an EFF-ANC coalition as likely at all (the market misunderstands the NEC’s views here and that they will avoid this at all costs) and an opposition ‘MPC’ coalition as more unlikely still. The baseline coalition outcome means status quo for policy (steady but slow reform), whilst DA involvement could lead to upside risks but would take time to emerge given constraints.

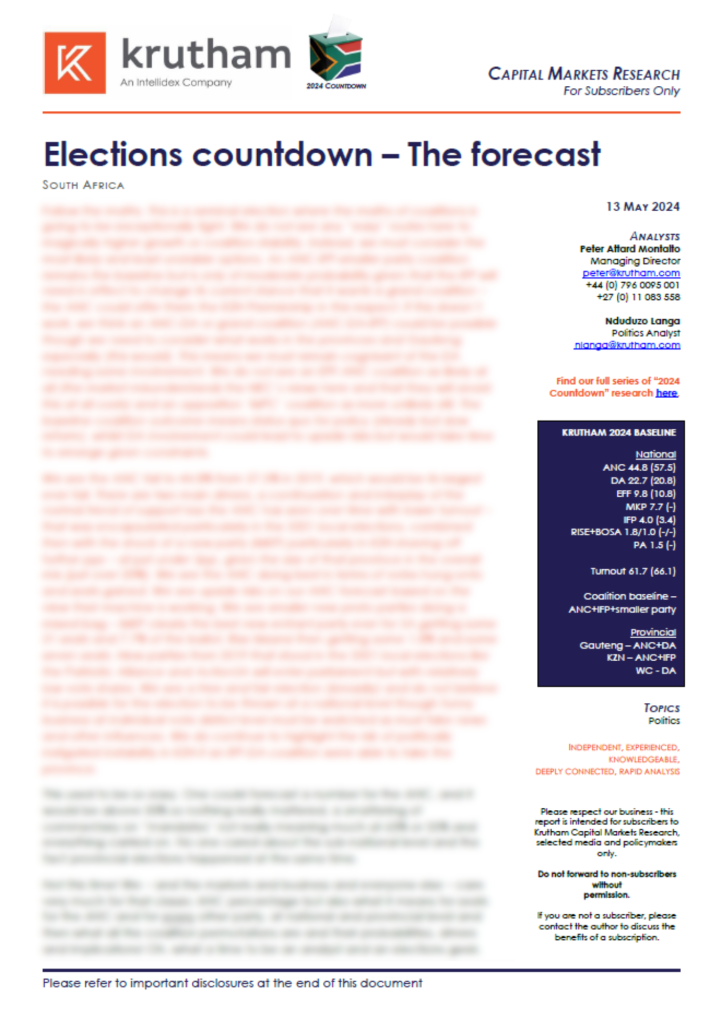

We see the ANC fall to 44.8% from 57.5% in 2019, which would be its largest ever fall. There are two main drivers, a continuation and interplay of the normal trend of support loss the ANC has seen over time with lower turnout – that was encapsulated particularly in the 2021 local elections, combined then with the shock of a new party (MKP) particularly in KZN shaving off further pps – at just under 5pp, given the size of that province in the overall mix (just over 20%). We see the ANC doing best in terms of votes hung onto and seats gained. We see upside risks on our ANC forecast based on the view their machine is working. We see smaller new proto parties doing a mixed bag – MKP clearly the best new entrant party ever for SA getting some 31 seats and 7.7% of the ballot, Rise Mzansi then getting some 1.8% and some seven seats. New parties from 2019 that stood in the 2021 local elections like the Patriotic Alliance and ActionSA will enter parliament but with relatively low vote shares. We see a free and fair election (broadly) and do not believe it is possible for the election to be thrown at a national level though funny business at individual vote district level must be watched as must fake news and other influences. We do continue to highlight the risk of politically instigated instability in KZN if an IFP-DA coalition were able to take the province.

These are the first elections where investors and markets really care about the sub-national level. With its intensified pursuit of the devolution of powers, the DA-led Western Cape has provided a preview of what the loss of power in more provinces and municipalities by the governing ANC may mean for policy making and the sharing of powers and functions between different levels of government after this election. The dominance of the ANC at all levels of government has minimised confrontations and struggles for power between national, provincial and local government. This state of harmony is being eroded (positively one would argue). As such, we foresee provinces and municipalities tussling in public and under the constitutional framework or such conflicts, with national government for more powers, especially to influence and make policy decisions that will serve the specific areas they govern. While this may not happen immediately after the 2024 elections, it is likely to intensify after the municipal elections in 2026 and beyond.

That said, post-2024 elections we foresee the Western Cape province, which is in sync with municipalities in the province due to being governed largely by the same party, continue to pursue more powers as the Western Cape Provincial Powers Bill symbolises. Should Gauteng fall to an ANC-led coalition, we expect much more noise and for it to pursue policies that will lead to the attempted establishment of provincial banks, the strengthening of the township economy, and employment programmes and will be a focus given the FDI in the province. Importantly, Mpumalanga will be focusing on the just energy transition (JET).

South Africa’s commitment to meet global climate goals aligned to the Paris Agreement is complicated by the country’s energy crisis which generates fraught contestations about what the country’s priorities should be. As such, political parties’ energy and climate change policies reflect an attempt to balance the immediate need for energy supply security and South Africa’s decarbonisation target (as well as vested interests). The challenge for parties lies in deciding on the most prudent approach concerning costs and time to resolve load shedding as quickly as possible. The key argument centres around the required energy mix, with some parties wanting a balance of renewables and fossil fuels, and others wanting fossil fuels excluded. All the parties we cover in this note agree on the need for a solution to load shedding as well as the imperative to transition to renewable energy as part of efforts to decarbonise and mitigate against the severity and impact of climate change. Their approaches however reveal certain biases for vested interests that are enmeshed – in particular the ANC.

The African National Congress (ANC) holds a balanced view of the two imperatives but understandably shows a strong bias for resolving load shedding and vested interests. As such, it sees a balanced mix of renewables, coal, nuclear and gas. Coalitions may complicate energy and climate change plans. However, an ANC-smaller parties coalition would see the status quo retained and we expect that the ANC’s internal contestations over this would be moderated. ActionSA calls for a transition to renewables while cautioning that this should be done in an economically responsible manner. In the short-term, it sees Eskom reform as the key to solving load shedding. ActionSA’s proposals do not vastly differ from those of other parties and would therefore be easily incorporated into a coalition government’s plans. The Democratic Alliance (DA) is the only party that demonstrates a pronounced bias for renewables and firm decarbonisation over all horizons. In a coalition context, it would be difficult for the DA to transition the country in a manner and pace it intends to. The Economic Freedom Fighters (EFF) demonstrates a heavy bias for “clean” coal and nuclear energy. An ANC-EFF coalition, which is one of the limited ways that the EFF could be in government after May 29, may see government embracing nuclear and (clean) coal more at a policy level. Practically, the EFF’s plans in relation to nuclear and coal will be difficult to implement and may therefore not amount to much. The Inkatha Freedom Party’s (IFP) views are balanced, with an unpronounced bias for coal and nuclear. The IFP’s plans show greater flexibility and would be implementable in most feasible coalition scenarios but the party’s position within a coalition would work against this.

In this note, we delve into party views on the social wage which plays a crucial role in cushioning the impact of inequality, poverty, and unemployment on citizens, but is paid for by a narrow tax base. Political party views on the social wage will have implications for the fiscus due especially to the lack of easy new funding options and the challenge of raising taxes in a coalition environment.

The social wage is a contentious topic, partly because it constantly receives the largest share of non-interest expenditure at 60%. That said, among parties there is consensus on the need to retain and expand the social wage, and social grants in particular, due to the role they play in dignifying the lives of a large section of the population. The ANC holds a more optimistic view of the social wage. For instance, in substantiating its call for a basic income grant, the party argues that people aged between 18 and 59 should have access to a grant just as children and the elderly do, while other parties are wary of perpetual dependence on social grants. While appreciating the need for social grants and arguing for their expansion, the DA, IFP and ActionSA emphasise the need for economic growth to ensure that only a few need social grants. Parties also support the idea of universal healthcare coverage but generally oppose the National Health Insurance in its current proposed form, with only the ANC supporting it.

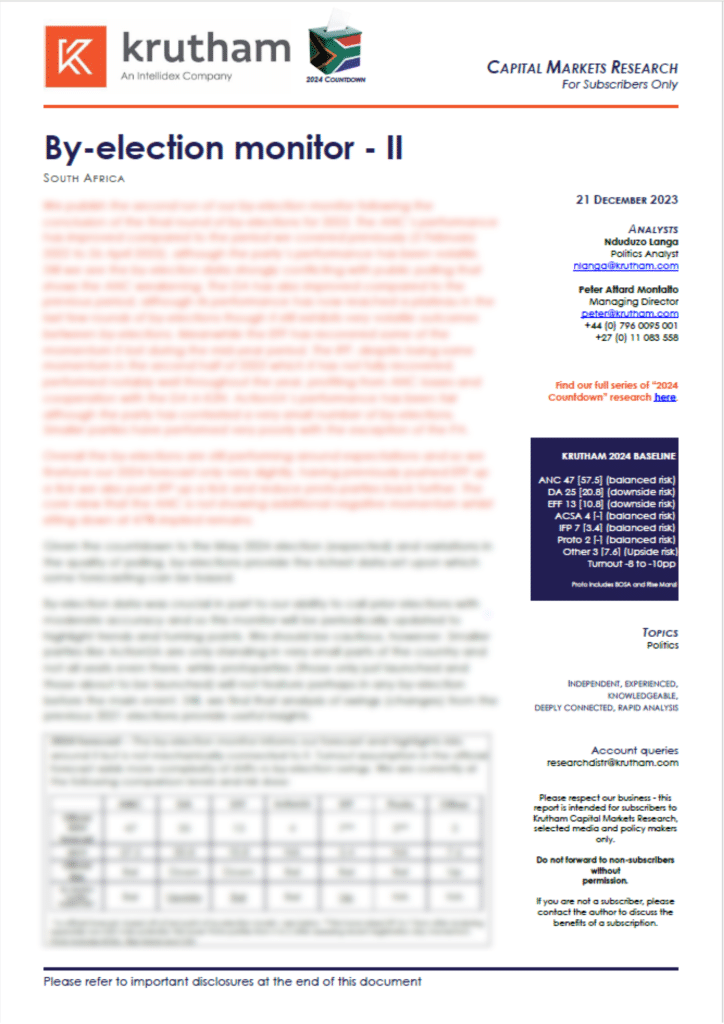

We publish the second run of our by-election monitor following the conclusion of the final round of by-elections for 2023. The ANC’s performance has improved compared to the period we covered previously (2 February 2022 to 26 April 2023), although the party’s performance has been volatile. Still we see the by-election data strongly conflicting with public polling that shows the ANC weakening. The DA has also improved compared to the previous period, although its performance has now reached a plateau in the last few rounds of by-elections though it still exhibits very volatile outcomes between by-elections. Meanwhile the EFF has recovered some of the momentum it lost during the mid-year period. The IFP, despite losing some momentum in the second half of 2023 which it has not fully recovered, performed notably well throughout the year, profiting from ANC losses and cooperation with the DA in KZN. ActionSA’s performance has been fair although the party has contested a very small number of by-elections. Smaller parties have performed very poorly with the exception of the PA.

Overall the by-elections are still performing around expectations and so we finetune our 2024 forecast only very slightly, having previously pushed EFF up a tick we also push IFP up a tick and reduce proto-parties back further. The core view that the ANC is not showing additional negative momentum whilst sitting down at 47% implied remains.

Given how high the stakes will be in the 2024 elections, parties may be tempted to use whatever means at their disposal to mobilise support, including xenophobia. South Africa has a history of xenophobia which has manifested itself in several, periodic xenophobic attacks. As such, the ground is fertile for attempted xenophobic political mobilisation. Parties that have placed immigration issues at the centre of their identity and political message have grown both in strength and number since the 2019 elections. As such, there will be some significant anti-immigration messaging and noise. However, the bigger parties tend to avoid campaigning explicitly on immigration issues, meaning that although “anti-immigration parties” have grown, immigration issues will not decide the election. The ANC may battle to break this trend though. Importantly, xenophobic violence typically does not occur during election season, only after, and we expect this trend to persist in 2024.

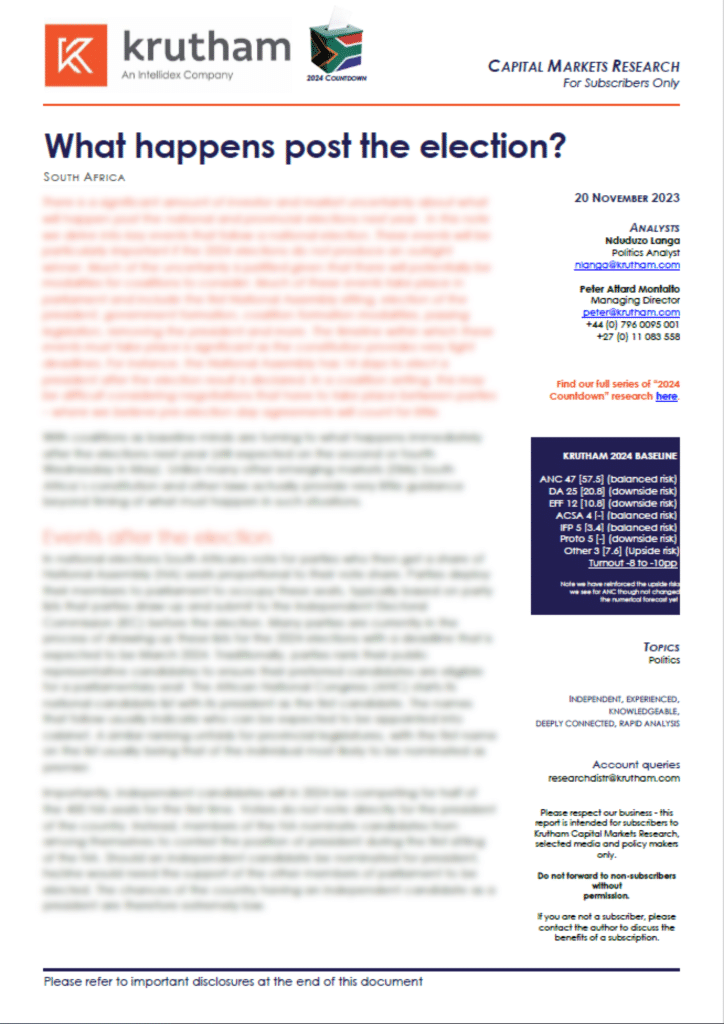

There is a significant amount of investor and market uncertainty about what will happen post the national and provincial elections next year. In this note we delve into key events that follow a national election. These events will be particularly important if the 2024 elections do not produce an outright winner. Much of the uncertainty is justified given that there will potentially be modalities for coalitions to consider. Much of these events take place in parliament and include the first National Assembly sitting, election of the president, government formation, coalition formation modalities, passing legislation, removing the president and more. The timeline within which these events must take place is significant as the constitution provides very tight deadlines. For instance, the National Assembly has 14 days to elect a president after the election result is declared. In a coalition setting, this may be difficult considering negotiations that have to take place between parties – where we believe pre-election day agreements will count for little.

Recent developments indicating a possible and impending termination of the relationship between the ANC and the EFF in municipalities they govern together have reignited an interest in the (in)stability of metros (though it is taking the ANC some time given the drama that is likely to follow). In addition, the DA is preparing to table a motion to dissolve the City of Johannesburg council. In this note, we provide an update on the latest political developments across metros in the country. Generally, metros have enjoyed a period of political stability in recent months (though the same cannot quite be said for service delivery), despite isolated events which have threatened the incumbency of some leaders. Removing the EFF however will leave four major metros in the lurch – though the ANC seems to think the impending dysfunction outweighs the risk of being associated with the EFF (a risky gamble). While attention is presently shifting towards metros as they get caught up in 2024 electioneering, we expect attention to shift away from them once parties start publishing their manifestos.

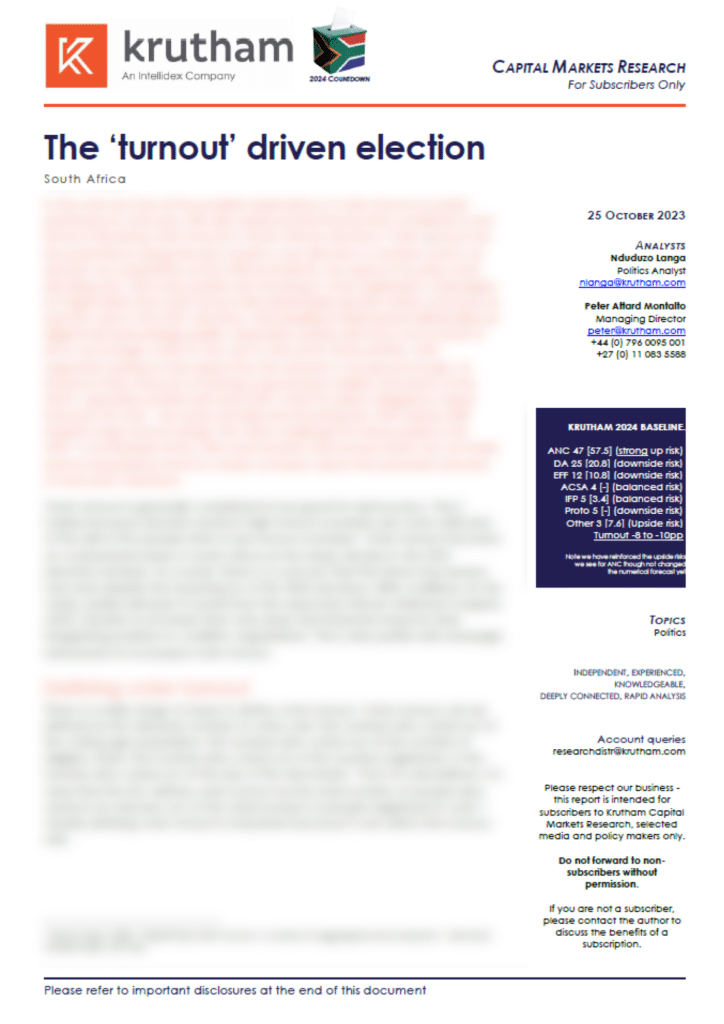

In this note we look at the possible implications of voter turnout on party performance next year. We also assess several factors that contribute to the trend of declining voter turnout in South African elections. Voter turnout has the potential to swing election results in one direction or another and in an election as competitive as the 2024 poll will be, we expect it to play a key deciding role. This is why parties are investing in voter registration campaigns. It is highly likely that voter turnout will substantially decline further next year as was the case in the 2021 elections. Our baseline is that turnout will decline by eight to ten percentage points. Opposition parties will have a lot of work to do to encourage voters to turn up to vote as for these parties, ANC supporters opting to stay away from the election is not good enough. To enhance their chances of forming a governing coalition (exclusive of the ANC), opposition parties will need ANC voters to switch allegiance rather than just not vote – we show actually why knocking the ANC below 50% requires huge turnout swings. The other challenge for these parties is the ANC’s countrywide reach. We must mention that surveys which do not make turnout assumptions tend to create confusion about the potential outcome of next year’s elections.

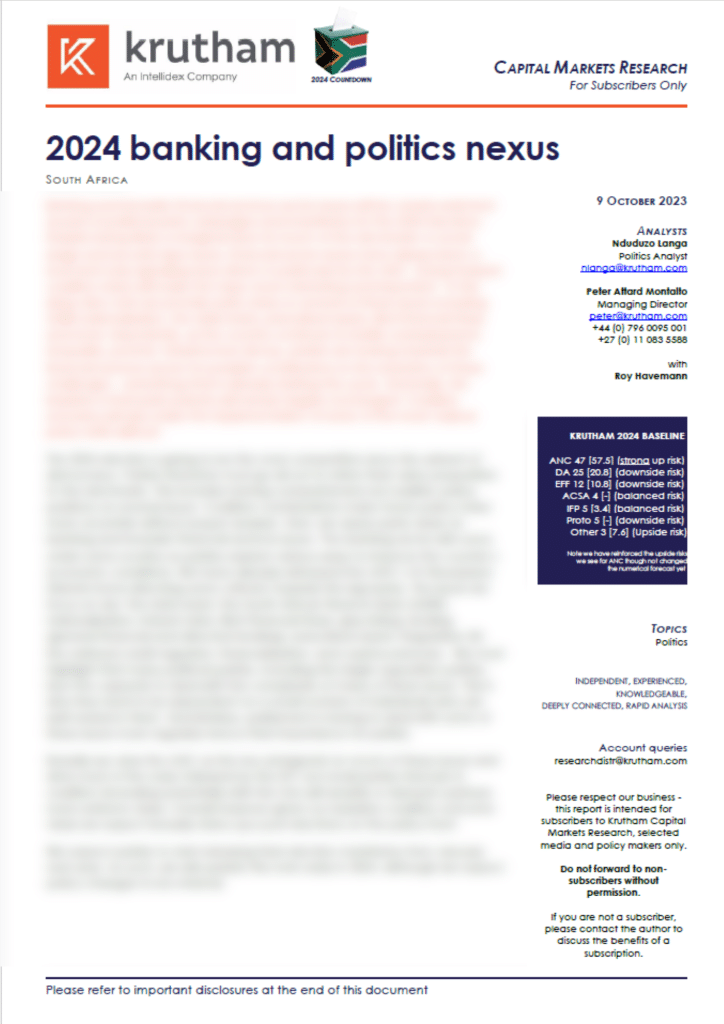

Banking and broader financial services sector issues will be closely watched as part of political party campaigns and manifestos for the 2024 elections. Despite being likely a marginal issue for much of the electorate vs social wage and security type issues, financial sector issues have always been a loud and noisy signalling issue driven in particular by the ANC. Going forward coalition mixes will make the topic more interesting and important. In this deep dive note we provide party views on several of these issues including SARB nationalisation, the state bank, prescribed assets, illicit financial flows and more. Importantly, as the country continues to battle unemployment, inequality, poverty, infrastructure decay, parties are looking towards the financial services sector for possible contributions to the resolution of these challenges – something that is already starting this cycle. Generally, the baseline is that party policies will remain largely unchanged. Coalition scenarios will also make the implementation of some of the more radical policy shifts difficult.

Parties need a substantial amount of funds to run their campaigns for the elections in 2024 yet the Political Party Funding Act is creating problems. The contestation over the Act will only intensify as parties seek easier ways of sourcing funding as they prepare for the most significant poll since the advent of democracy. We suspect however that funds are finding their way into a myriad of different routes to deploy capacity to parties – though we do not believe there is major influence over bread-and-butter policy issues, there may well be over issues like coalition formation modalities.

Despite the existence of the Act which came into effect in April 2021, the discourse about the transparency of political party funding continues. Calls for the Act to be amended have surfaced from both stakeholders who want to see it becoming more stringent and those who want it to be relaxed. As strong as the cases for either of these calls are, we do not see significant amendments taking place before the 2024 elections.

The contestation about the act centres on four issues: the ZAR100,000 threshold for disclosure; the ZAR15m upper limit that a donor can donate to a party in a year; foreign donations; and donations from the same source of wealth and usage of multiple entities to donate above the upper limit. What is clear is that none of the parties to the contestation will achieve a clear victory over the other. Moreover, amendments aimed at relaxing the act will face a legal challenge from civil society which has been at the forefront of the campaign for transparency on political party funding. As such, for the first time in national and provincial elections, parties’ funds will be limited by the Act. For those parties that do not maintain a permanent presence in certain sections of the country, campaigning in these areas will be difficult due to limited resources. The solution for parties would be to seek funding from multiple donors rather than just their traditional donors.

The Social Research Foundation (SRF) has conducted several polls on a variety of issues that concern South Africans, providing some insight into public opinion which is important especially in this period leading up to elections. These issues include loadshedding, emigration and immigration, coalitions and more.

In this note, we zoom into some interesting findings from these surveys which typically poll registered voters. While this approach is reasonable as it is more likely to shed light on the views that will be expressed in the 2024 elections, it does not include the opinions held by those not registered to vote. Moreover, the voter registration process is ongoing and the voters’ roll may look different in May next year (when elections are expected to be held) to how it looks now or when some of these polls were conducted.

Overall, from the SRF’s insights we can conclude that the DA still suffers from perceptions that it caters to the needs of a minority of citizens. As such, we should not expect a direct swing of votes from the ANC to the DA in 2024. We are also able to conclude that the EFF suffers from perceptions that it is violent and spreads hate. We therefore do not expect a dramatic improvement in the party’s electoral fortunes next year. All this means that despite its evident shortcomings, the ANC should not be written off as some voters still express support for the party, even in the face of challenges such as loadshedding.

The IFP will be an important part of the coalition conversation after the 2024 national election. With the party appealing to both the ANC and the DA, there is a significant probability that it would be part of a coalition government if next year. The IFP is primarily, historically, known as the ANC’s nemesis in KZN. For the older generations, the party is also infamous for its role during apartheid, in particular its conflict with the ANC. Given its importance and its rather limited publicity in comparison to even some of the newer parties, we take a deep dive into the IFP. Our primary concern is dissecting the various factors that may determine the party’s position after the 2024 elections. The IFP currently has 14 seats in the National Assembly, in line with its 3.38% vote share. The ANC’s 57.50% victory saw it occupying 230 seats. In 2024, we expect the IFP to improve to around 5%, and the ANC to decline to about 47%. This makes a coalition between the two parties feasible and would be less contentious than other coalition scenarios. The main threat to the coalition would be that the IFP in KZN still views the ANC as a direct rival in the polls (and is doing very well there at the ANC’s expense). The sporadic usage of undiplomatic language between the IFP and ANC demonstrates this point. However, the two parties’ deliberate efforts to reconcile as exemplified by cooperation in government in the early days of democracy have normalised relations to a great extent. Yet added to the mix is the IFP’s new closeness at a principal level to the DA. This all demonstrates that the IFP’s coalition position is much more complex than many may want to believe and than the media often assume. Overall whilst we think a national ANC/IFP coalition is of decent probability (and could see the ANC pressure the IFP to keep them in power in the province too) a split of control in the

province keeps things uncertain.

As 2024 election-related activity gradually intensifies, we get a sense of the narratives that will dominate different political parties’ campaigns. With various challenges currently confronting the country there are thematic issues that transcend party lines, and some parties even agree on solutions – the gaps are maybe not as much as expected. There are also issues which are more important to certain parties than others. This is due to a variety of factors including the history, ideology, and the core section of the electorate that a party represents. One thing which is clear is that parties are generally in support of greater private sector involvement on solutions to various

challenges that the country faces. While this is a positive trend, it also confirms that parties are unable to foresee how any other government would be able to undo some of damage that the incumbent government has done to various sectors of the country. Exceptions to this support for the private sector are found in the policies of both the EFF and the ATM, although the latter’s stance is not as inflexible as that of the former.

Policy issues will be important to some degree as coalition agreements must be negotiated after the elections – though the election shifts will only be on policy issues in a small part. In this note we zoom into the policies of the top five parties, in accordance with the 2019 national election results. We also touch briefly on ActionSA which has shown some growth potential. We do the same for some of the smaller and newer parties with potential to grow. Overall, the policy landscape still needs some refining as we move towards manifesto launches in January. Notwithstanding, parties demonstrate an increased focus on energy issues given the energy crisis the country currently faces. Apart from the EFF, parties are generally in favour of more private sector involvement in energy and other sectors of the economy. The ANC’s message is complicated by the divergent views and voices that exist within the party, which are better understood by investors than the divergence in other parties. However, that the party is in government helps in ascertaining certain positions, even though these positions at times only exist on paper.

The ANC’s performance has improved, meaning that there is now greater focus on the possibility of the party winning just over 50% of the vote next year – though our baseline remains that they get just below at 47% but we have shifted the risk skew. The DA’s general performance has been fair, but not particularly impressive, while the EFF should be recognised for attempting to register its presence in all parts of the country. The IFP will be satisfied with its performance in recent by-elections while both ActionSA and the PA have the potential to grow nationally.

This is the first of these monitors we will publish roughly every two months or as major trends and turning points develop into the 2024 elections.

It is now widely accepted that the 2024 elections may introduce coalition governments at national and provincial levels (Gauteng in particular) – and equally widely accepted that this is going to be, at best, a mixed blessing. Markets have given up on the idea this is necessarily a positive route to reform. Given the dysfunction and instability that has engulfed many coalitions and coalition-governed municipalities, there is general concern that such disorder and uncertainty may characterise national and provincial governments after the 2024 elections. Operating on the premise that a need for coalition governments will arise in 2024, we explore various possible and

realistic compositions of coalitions that may govern the country after the 2024 elections. We restrict our exploration to the national level. At this stage, our primary concerns centre on the stability of a coalition as well as the ramifications that the formation of that coalition would have for overall economic policy direction. Most possible coalitions would be a nightmare for both coalition partners and the country. The most likely coalition to assume power is that of the ANC and minority parties (including the IFP). This coalition would have the least number of contestations as smaller parties tend to lack the resources to make significant policy contributions – and policy status quo would largely continue. This is likely the first of several iterations of this report as we move towards and then after the elections.

The Democratic Alliance’s recently concluded federal congress took place during a time of considerable preoccupation with how opposition parties will fare in next year’s elections. Despite being the second-largest party and having a defined ideological posture, the party has found it difficult to drive home to voters its position and role in South African politics as the political landscape undergoes consistent change. It is also struggling to get a particular type of ANC voter and even non-voters to swing to the DA. We delve into these and other issues as we assess the factors that could determine how the DA fares in 2024 and beyond – including problems of being overstretched in terms of capacity, centralised control, unstable coalition management, and prioritising purity of view over support.

Since its formation, the DA has experienced gradual growth which has attracted various political leaders. That diversity of leaders has resulted in divergent views on the direction that the party should pursue. This is normal for a party that is experiencing growth and therefore venturing into new territories – albeit with limited success. The party has, however, struggled to handle the increasing multiplicity of views within its ranks. This has resulted in an exodus of leaders and muted electoral gains. Maintaining the gradual growth after problems in Gauteng (explained below) may be tricky. Yet in KwaZulu-Natal the DA is showing slight momentum showing it would be a mistake to underestimate it.

The upshot is that the party has been concurrently everywhere and nowhere. It is trying to consolidate its core base while simultaneously seeking to grow its support. Solving this conundrum, at least temporarily, through the formation of a “moonshot pact” with other opposition parties for 2024 may be a step too far, yet a DA coalition with the ANC might self-destruct both parties. We see them getting slightly higher than the last election next year but on markedly lower turnout.

The observable failures of different spheres of government and state parastatals to fulfil their mandates have attracted greater scrutiny towards the governing party’s deployment practices. As such, the constitutionality, desirability, and effectiveness of the African National Congress’ (ANC) cadre deployment policy have been questioned frequently in recent times. This public discourse was amplified by the findings of the State Capture Commission (Zondo Commission) on the policy. So important is cadre deployment that the Democratic Alliance (DA) is currently embroiled in a legal battle with the ANC over the governing party’s deployment practices and access to its deployment committee records. In the context of pronounced inefficiencies of different government spheres and state institutions, it is important for us to examine various facets of cadre deployment. Given the public criticism that has been directed towards cadre deployment, we also explore the feasibility of a public service that is free of cadre deployment.

Paul Mashatile had long been identified as the frontrunner for ANC deputy presidency. This observation was solidified when he received the highest number of branch nominations. Mashatile went on to be elected ANC deputy president at the party’s 55th national conference. As we have indicated in some of our previous publications, Mashatile could succeed Ramaphosa, should he not finish his term as both the president of the ANC and the country, an eventuality that is now quite possible (though not baseline) considering the Phala Phala. We thus can expect Paul Mashatile to eye up the presidential seat towards the end of Ramaphosa’s second term, especially if Mashatile stands for ANC presidency in 2027 and gets elected. We expect Mashatile to be on manoeuvres already, though the 2024 elections may keep this on the backburner for now. He will also try to transition to state Deputy President as quickly as possible, though the ANC will not want to be seen to be rushing it. Mashatile is therefore an important figure, worthy of scrutiny. We find him moderately status quo and a pragmatist of the conservative centre left on the surface on a range of policy issues (though he is not a policy wonk) but scratching below the surface underlying motives of both him and his wider ecosystem need to be kept in mind with a sceptical eye. We must wait to see if suspected, rumoured dirt does start to emerge from investigative journalists as his rise continues, though the ability of others in the ANC to take him out with dirt has not happened still and might risk bringing a huge chunk of the Gauteng ANC down. As state Deputy President he would have an interesting opportunity to prove himself, though there is little from his history to suggest he can turn capacity issues in the post-peak-state-capture world. Still being urbane and with decent PR he is someone the private sector will find very interesting.

With South Africa rapidly moving away from being a one-party dominant state, opposition parties have become central to the functioning of the country, and it is therefore important that more literature on these parties is produced. Specifically, we dissect the third largest party in the country, the Economic Freedom Fighters (EFF) which has the capacity to generate far more noise and uncertainty than other opposition parties. The EFF has recently made headlines for switching alliance from the DA to the ANC and vice versa. We seek to unpack the party’s fluid positions in relation to coalitions and coalition partners. Our aim is to provide a detailed scrutiny of the EFF’s trajectory. We then use this dissection to zoom into the role that the EFF will play in South African politics in the future, given the upcoming 2024 general elections and the party’s potential to further alter South African political dynamics through forming coalitions in particular with the ANC. We caution overall that the party will add much drama but stereotypes about how they may behave on policies and reforms in particular should be treated with great caution.

The decline in electoral support for the ANC has necessitated the formation of coalition governments in several municipalities across the country. Coalition governments, particularly in metros as exemplified by events in Johannesburg and Ekurhuleni in 2022, are susceptible to instability as bigger parties battle for control. An often-overlooked aspect in discourse around coalitions is the role that minority parties play in the (in)stability of municipalities governed by coalition governments. With the highly anticipated 2024 national and provincial government elections in mind, we take a closer look at the role that these parties play in municipalities, especially in as far as stability is concerned. Our focus is going to be mainly on the post-2021 local government elections (LGE) period, as well as metropolitan municipalities, due to these municipalities’ importance to the overall functioning of the country.